Marketplace Individuals Recognise Atea Prescription drugs, Inc.’s (NASDAQ:AVIR) Earnings Pushing Shares 28% Bigger

Earnings Pushing Shares 28% Bigger")

The Atea Prescribed drugs, Inc. (NASDAQ:AVIR) share value has carried out really perfectly around the final month, putting up an exceptional gain of 28%. Still, the 30-working day jump would not change the truth that extended expression shareholders have witnessed their stock decimated by the 61% share value drop in the last twelve months.

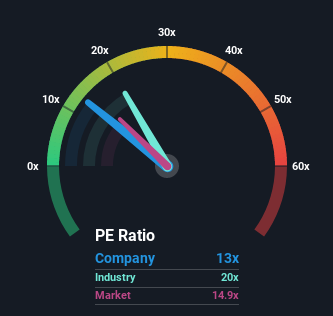

Though its value has surged increased, there nevertheless would not be a lot of who feel Atea Pharmaceuticals’ rate-to-earnings (or “P/E”) ratio of 13x is really worth a point out when the median P/E in the United States is comparable at about 15x. Nevertheless, investors may possibly be overlooking a very clear prospect or probable setback if there is no rational foundation for the P/E.

Atea Pharmaceuticals could be executing much better as its earnings have been likely backwards currently while most other companies have been viewing positive earnings expansion. It could possibly be that a lot of count on the dour earnings functionality to fortify positively, which has kept the P/E from falling. If not, then current shareholders may be a tiny nervous about the viability of the share price tag.

See our most up-to-date evaluation for Atea Prescribed drugs

If you’d like to see what analysts are forecasting heading forward, you really should examine out our totally free report on Atea Prescription drugs.

What Are Advancement Metrics Telling Us About The P/E?

The only time you would be cozy viewing a P/E like Atea Pharmaceuticals’ is when the firm’s growth is tracking the industry carefully.

Retrospectively, the previous calendar year delivered a frustrating 2.5% reduce to the firm’s bottom line. This has erased any of its gains for the duration of the previous 3 decades, with nearly no transform in EPS becoming achieved in total. So it seems to us that the corporation has had a combined end result in phrases of developing earnings about that time.

Shifting to the future, estimates from the four analysts covering the business advise earnings must develop by 9.4% each and every year around the future 3 decades. Meanwhile, the rest of the sector is forecast to increase by 11% every single year, which is not materially distinct.

With this details, we can see why Atea Pharmaceuticals is investing at a fairly equivalent P/E to the industry. Apparently shareholders are comfy to basically keep on whilst the firm is retaining a very low profile.

What We Can Find out From Atea Pharmaceuticals’ P/E?

Its shares have lifted significantly and now Atea Pharmaceuticals’ P/E is also back up to the market place median. Typically, we might caution versus studying also significantly into rate-to-earnings ratios when settling on expense decisions, although it can expose lots about what other market participants feel about the firm.

We’ve established that Atea Prescribed drugs maintains its average P/E off the again of its forecast progress staying in line with the wider market, as envisioned. At this phase buyers feel the likely for an advancement or deterioration in earnings isn’t terrific ample to justify a superior or low P/E ratio. It is difficult to see the share cost moving strongly in both direction in the in the vicinity of long term below these instances.

It is also really worth noting that we have located 1 warning signal for Atea Pharmaceuticals that you want to take into thing to consider.

You might be in a position to locate a superior investment than Atea Prescription drugs. If you want a range of achievable candidates, examine out this cost-free listing of attention-grabbing businesses that trade on a P/E down below 20x (but have verified they can grow earnings).

Have feed-back on this write-up? Worried about the content material? Get in contact with us immediately. Alternatively, electronic mail editorial-group (at) simplywallst.com.

This article by Just Wall St is standard in nature. We give commentary centered on historical details and analyst forecasts only working with an impartial methodology and our content articles are not supposed to be monetary assistance. It does not represent a recommendation to get or offer any inventory, and does not take account of your goals, or your economic condition. We purpose to bring you extensive-phrase focused evaluation pushed by basic info. Observe that our analysis might not issue in the hottest selling price-delicate business bulletins or qualitative material. Only Wall St has no place in any stocks stated.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/2IL6CD67CJOEBGSQREMOJL2X2I.jpg "Alzheimer’s drug study yields constructive benefits, say makers Eisai and Biogen")