Rigel Prescribed drugs Inventory: A Position Check out (NASDAQ:RIGL)

")

vdvornyk/iStock by way of Getty Pictures

“Transfer to a new place and you promptly see that viewing a put as a tourist, and in fact transferring there for superior, are two pretty unique factors.” – Tahir Shah

Today, we glimpse in on Rigel Prescription drugs (NASDAQ:RIGL) for the to start with time because we did a piece on this biotech corporation again in mid-May possibly of last 12 months. It comes up in responses from In search of Alpha followers from time to time, so it seemed an acceptable time to revisit Rigel. A entire investigation follows under.

Trying to find Alpha

Enterprise Overview:

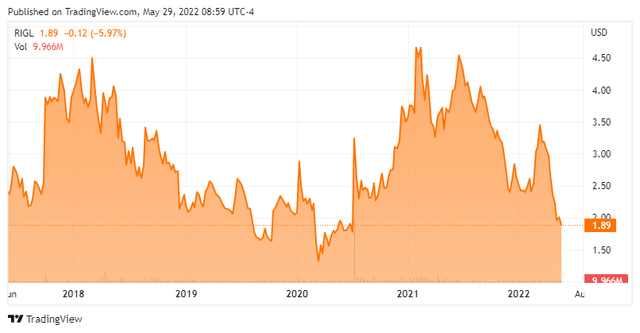

Rigel Prescribed drugs is based out of San Francisco. The corporation is targeted on acquiring compact molecule medicines to handle hematologic conditions, cancer, and exceptional immune health conditions. The company has a person drug on the current market termed Tavalisse. This is an oral spleen tyrosine kinase inhibitor for the treatment method of adult individuals with persistent immune thrombocytopenia. The inventory at this time trades just below two bucks a share and sporting activities an approximate marketplace capitalization of $310 million.

May Company Presentation

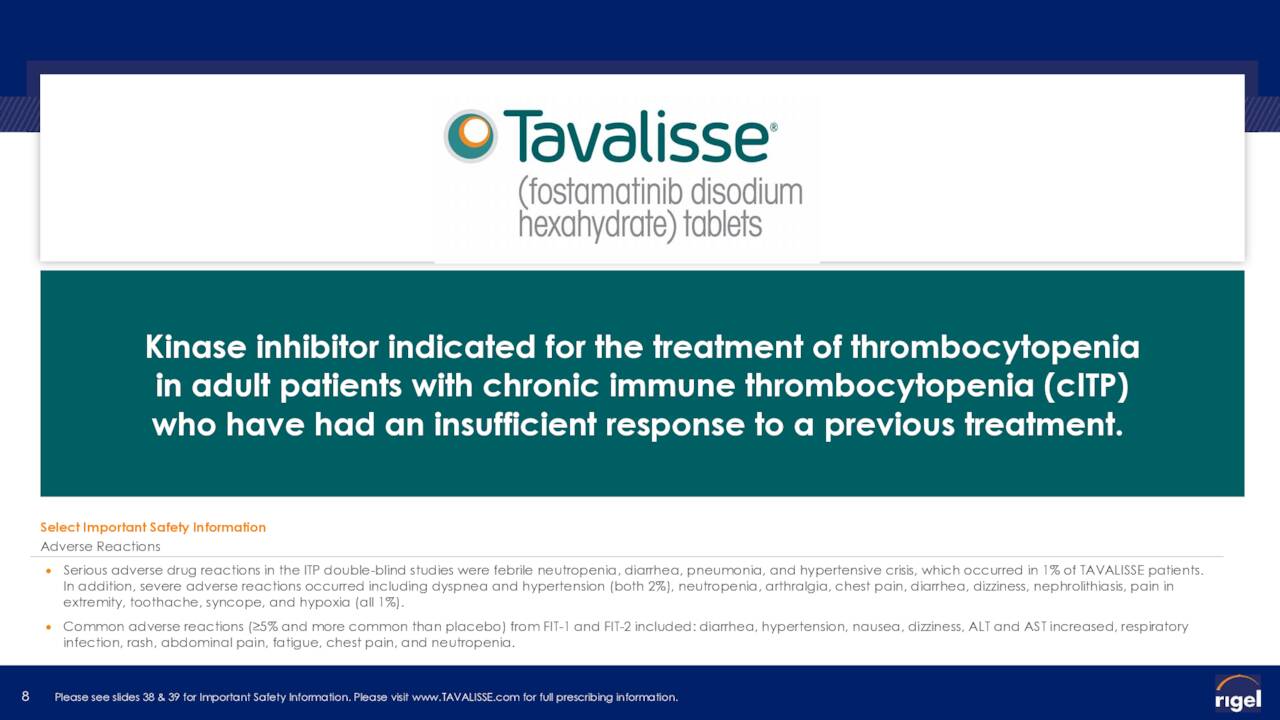

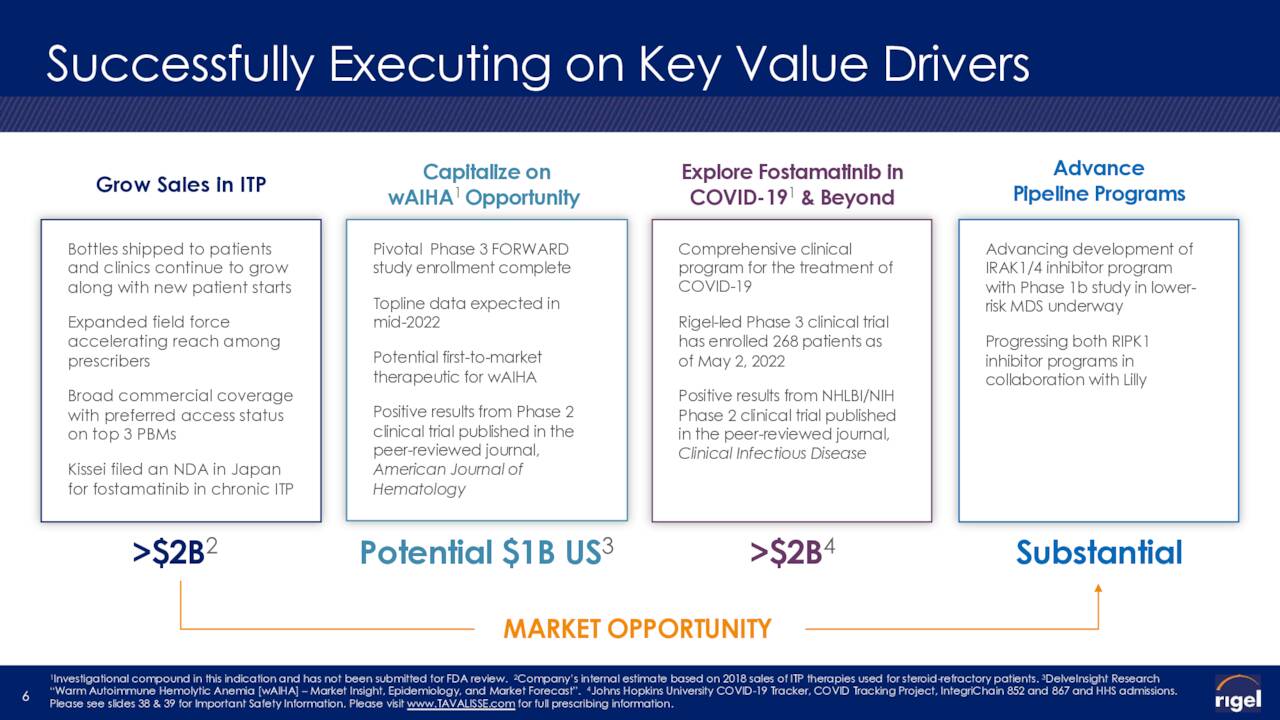

The enterprise has 1 authorized products referred to as Tavalisse (fostamatinib disodium hexahydrate) for the remedy of serious immune thrombocytopenia or CITP. Tavalisse did just somewhere around $63 million in web item gross sales for this indicator in FY2021. For the comprehensive yr, the business did virtually $150 million in all round revenues. However, just more than $86 million was agreement revenues, of which $66.6 million was via a collaboration with Eli Lilly which we will talk about later on in this post.

The drug was initial authorized for this indication in 2018. CITP is an autoimmune disorder. This affliction results in the body’s immune program to assault blood platelets, leaving sufferers with minimal blood platelet depend, and a propensity to bleed.

Might Business Presentation

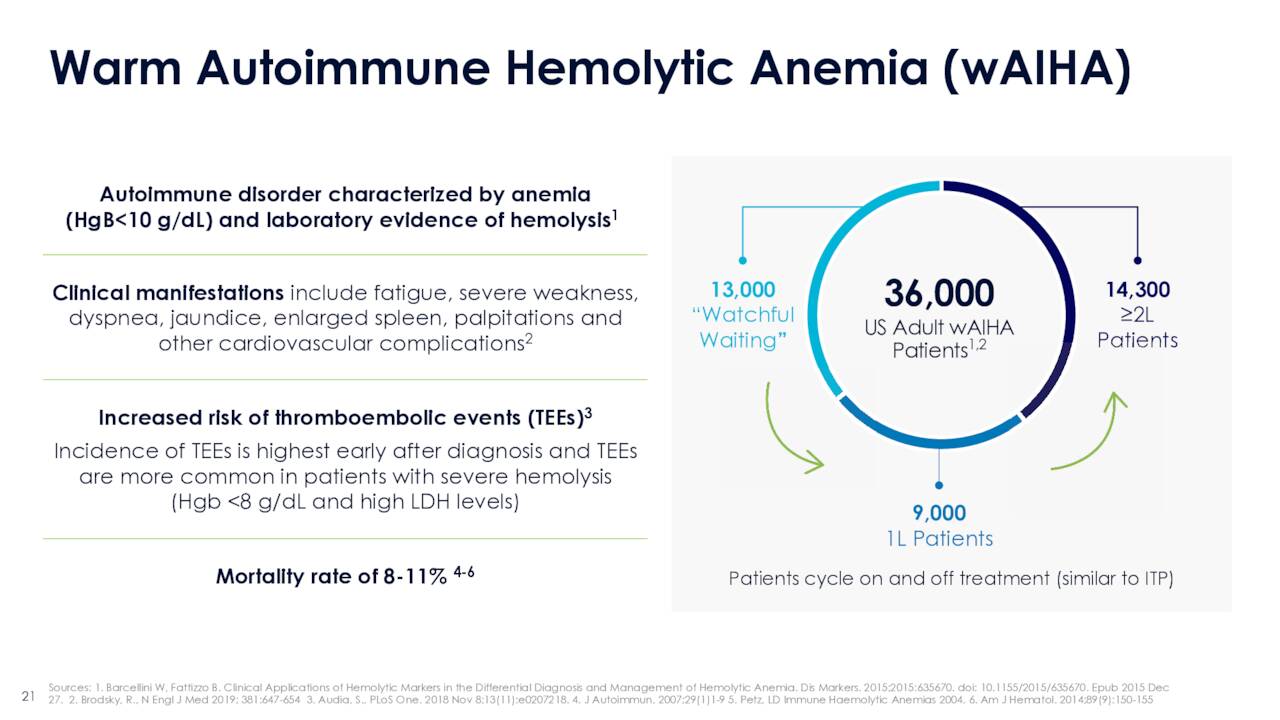

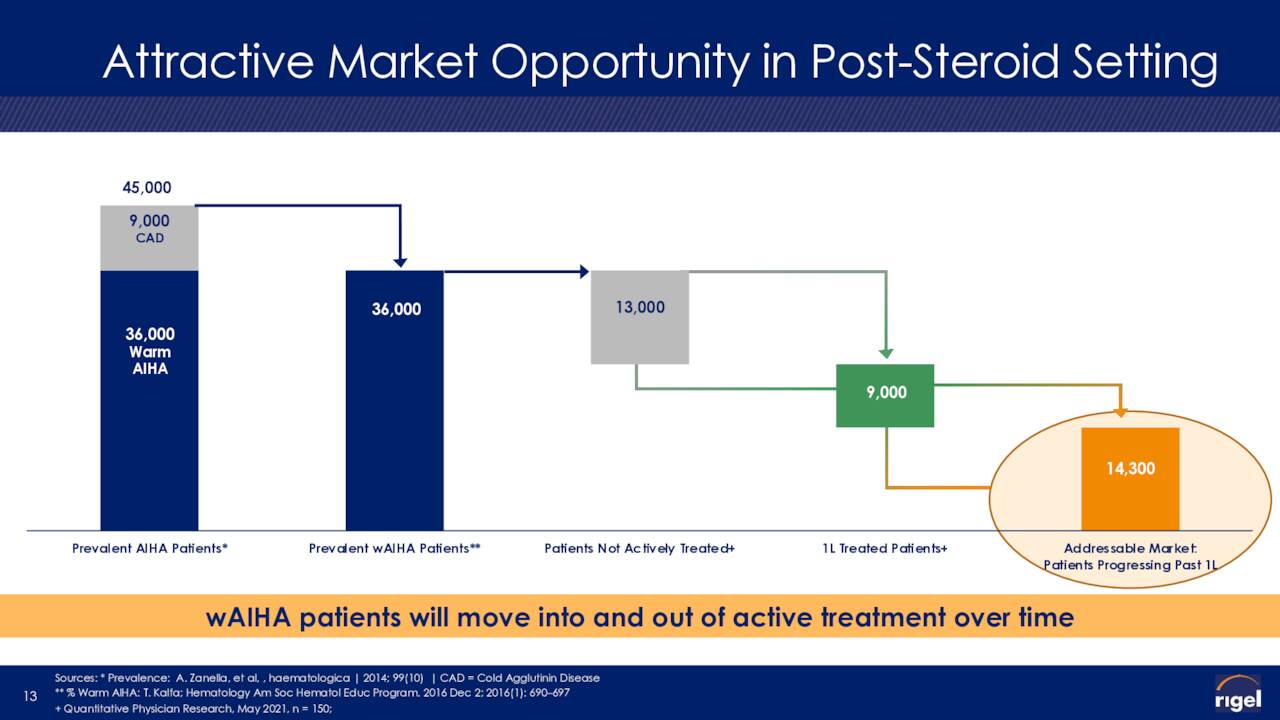

The corporation is also pursuing Tavalisse as a probable procedure for warm autoimmune hemolytic anemia or wAIHA. This is a serious blood disorder where by immune technique provides antibodies that consequence in purple blood mobile destruction, a equivalent approach as CITP. Topline benefits from a Period 3 analyze ‘FORWARD’ should really be out sometime this summer. There are no permitted therapies for this uncommon affliction and Tavalisse is concentrating on a subset of this group.

Might Organization Presentation

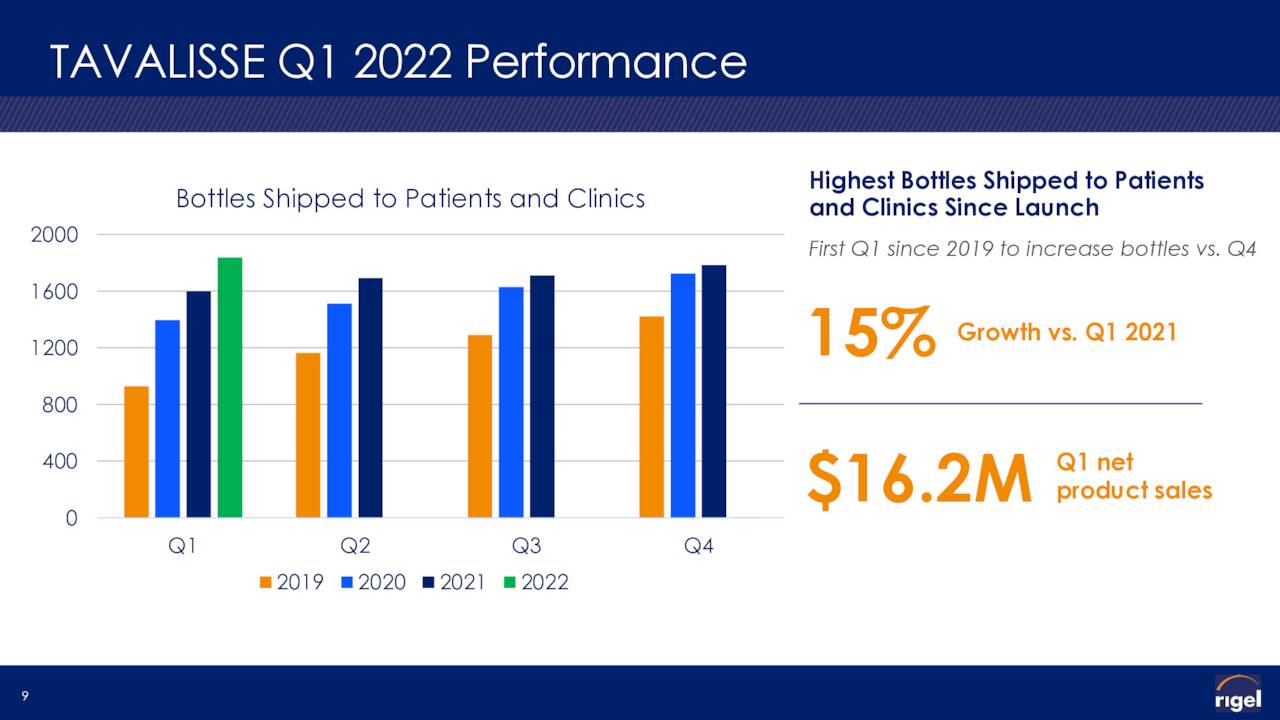

To start with Quarter Benefits:

In early May perhaps, Rigel posted initial quarter quantities. The company had a web GAAP reduction of 16 cents a share as revenues shrank just about 80% to just over $16.7 million. Both top rated and bottom line numbers a little bit skipped analyst anticipations. Revenues consisted of $16.2 million in TAVALISSE web product or service income and $.5 million in contract revenues from collaborations. The slide in revenues is totally due to the timing of contract revenues vis a vis 2021. Internet solution product sales of Tavalisse expanded decently in the quarter as some pandemic headwinds appear like they are commencing to ebb. Internet product or service product sales had been up some 30% from the $12.4 million the corporation posted for 1Q 2021. The company’s advertising lover Kissei Pharmaceutical has filed for internet marketing approval in Japan to handle CITP.

May possibly Firm Presentation

Analyst Commentary & Stability Sheet:

Proper just after very first quarter final results submitting, both equally BMO Funds and Citigroup reiterated Obtain rankings on RIGL with similar $7 price tag targets. H.C. Wainwright also reiterated its own Invest in score with a extra optimistic $11 price tag focus on.

The organization ended the initially quarter with dollars, hard cash equivalents and shorter-term investments of $107.5 million immediately after working with just around $17 million well worth of dollars for functions in the very first quarter. Roughly 4 per cent of the exceptional shares are at this time offered quick. The CFO acquired just over $105,000 truly worth of new shares on May well 22nd. It was the to start with insider exercise of any type in yrs in this fairness.

Verdict:

The latest analysis consensus has the firm’s net loss widening considerably to some 55 cents a share in FY2022 as revenues decline some 40% to around $90 million. Analysts hope that reduction to fall to just more than 30 cents a share in FY2023 as revenues increase nearly 50% to some $130 million.

May Enterprise Presentation

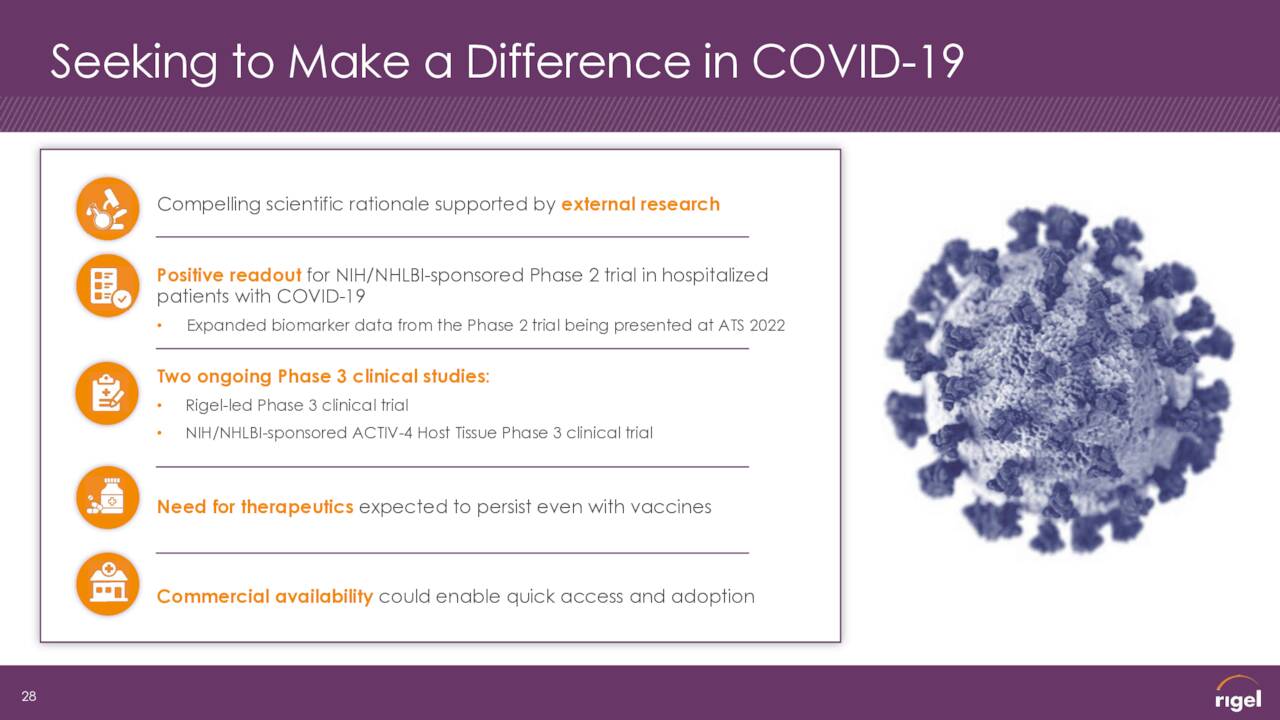

The business spelled out nicely the firm’s target places in excess of the upcoming 12-24 months through a new investor presentation. I individually put little benefit on the firm’s Covid-19 initiatives as I look at them as too little, much too late presented a lot of therapies previously on the market place as the pandemic ebbs. There have been several bullish content articles on these initiatives (I, II, III) about the past yr, but this initiative has not bolstered RIGL’s inventory rate to this level. To be reasonable, myriad little biotech/biopharma problems have pursued numerous Covid-19 solutions, the broad majority of which turned out to be fruitless. I would appreciate for Rigel to verify me wrong in this watch, but am not counting on it.

Could Company Overview

Its attempts exterior its main franchise are early phase and almost certainly are not germane to this evaluation possibly. It should really be noted that the company is associate with Eli Lilly (LLY) in just its RIPK1 portfolio which netted Rigel $125 million upfront payment early last yr. The business is also eligible for milestone payments totaling $835 million for the whole growth portfolio as effectively as tiered royalties contingent upon Rigel development financial commitment. An original Period 2 analyze in an immunologic condition indication is now expected to start in the first quarter of 2023.

This leaves product sales traction at Tavalisse getting the core around expression driver for the business. Both of those for its approved indicator as very well as development on the wAIHA front. I still like Rigel as an intriguing ‘sum of the components‘ tale. I proceed to keep my tiny ‘watch merchandise‘ holding in it via coated get in touch with positions, which I have ‘rolled‘ about a few of moments considering that my past article on this name. I would like to see a lot more development on reducing the firm’s quarterly income burn, stable review effects from the ‘FORWARD’ study and/or a beneficial progress on the Covid-19 entrance ahead of I insert to these holdings, nonetheless.

“He is unwell clothed, who is bare of virtue.” – Benjamin Franklin

/cloudfront-us-east-2.images.arcpublishing.com/reuters/2IL6CD67CJOEBGSQREMOJL2X2I.jpg "Alzheimer’s drug study yields constructive benefits, say makers Eisai and Biogen")